Capital budgeting is evaluating and selecting long-term investment projects or expenditures involving significant cash outflows. Various techniques can be employed when predicting future cash flows for capital budgeting purposes. Here are some common capital budgeting techniques used to estimate future cash flows:

Payback Period

The payback period is a capital budgeting technique that focuses on the time required to recover the initial investment made in a project. It is calculated by determining the period it takes for the cumulative cash inflows from the project to equal or exceed the initial cash outflow. The payback period is often expressed in years or months. One advantage of the payback period method is its simplicity and ease of use. It provides a straightforward measure of how quickly an investment will generate enough cash inflows to recover the initial investment.

This can be particularly useful for companies with liquidity concerns or those seeking to minimize the time it takes to recoup their investment. However, the payback period has several limitations. Firstly, it does not consider cash flows that occur after the breakeven point, which means it does not capture the project's profitability beyond the recovery of the initial investment. This can lead to a biased evaluation of projects with longer-term benefits. Secondly, the payback period fails to account for the time value of money, which is the concept that a dollar received in the future is worth less than a dollar received today.

By not discounting future cash flows, the payback period ignores the opportunity cost of tying up capital in the project and does not reflect the project's true value. Despite its limitations, the payback period can still be used as a preliminary screening tool to assess the liquidity and risk associated with an investment. It provides a quick measure of how long it will take to recover the initial investment, allowing decision-makers to gauge the project's time horizon for cash inflows. However, it is typically used in conjunction with other capital budgeting techniques, such as net present value (NPV) and internal rate of return (IRR), which consider the time value of money and provide a more comprehensive evaluation of a project's financial viability.

Net Present Value (NPV)

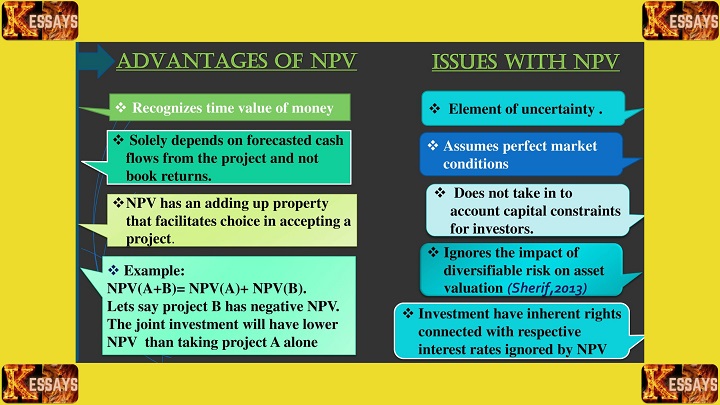

Net Present Value (NPV) is a widely used capital budgeting technique that takes into account the time value of money when estimating future cash flows. It calculates the present value of expected cash inflows and outflows associated with a project by discounting them using an appropriate discount rate.  The discount rate used in NPV is typically the company's cost of capital, which represents the minimum acceptable rate of return required for an investment. The discounting process reflects the idea that cash received in the future is worth less than the same amount of cash received today due to factors such as inflation and the opportunity cost of capital. To calculate NPV, the expected cash inflows and outflows are estimated for each period over the project's lifespan. These cash flows are then discounted back to their present value using the discount rate. The present values of the cash inflows are summed, and the present values of the cash outflows are subtracted from the total. If the resulting NPV is positive, it indicates that the project is expected to generate more cash inflows than outflows and is considered financially viable.

The discount rate used in NPV is typically the company's cost of capital, which represents the minimum acceptable rate of return required for an investment. The discounting process reflects the idea that cash received in the future is worth less than the same amount of cash received today due to factors such as inflation and the opportunity cost of capital. To calculate NPV, the expected cash inflows and outflows are estimated for each period over the project's lifespan. These cash flows are then discounted back to their present value using the discount rate. The present values of the cash inflows are summed, and the present values of the cash outflows are subtracted from the total. If the resulting NPV is positive, it indicates that the project is expected to generate more cash inflows than outflows and is considered financially viable.

A positive NPV implies that the project is expected to add value to the company, as it generates a surplus of cash inflows over the initial investment and the required rate of return. On the other hand, a negative NPV suggests that the project's expected cash outflows exceed the inflows, potentially indicating a value-destroying investment. NPV is a comprehensive capital budgeting technique as it considers the time value of money and accounts for all cash flows throughout the project's lifespan.

By incorporating the discount rate and the entire cash flow timeline, NPV provides a more accurate measure of the project's profitability and financial viability compared to simpler techniques like the payback period. When evaluating multiple investment options, projects with higher NPVs are generally preferred, as they are expected to generate higher returns and contribute more to the company's value. However, it is important to consider other factors such as project risks, strategic alignment, and qualitative aspects alongside NPV to make well-informed investment decisions.

Internal Rate of Return (IRR)

Internal Rate of Return (IRR) is another important capital budgeting technique used to evaluate the financial viability of investment projects. It is defined as the discount rate that makes the net present value (NPV) of a project equal to zero. In other words, it is the rate at which the present value of expected cash inflows is equal to the present value of cash outflows. To calculate the IRR, the cash inflows and outflows associated with the project are estimated for each period, similar to the NPV calculation. The IRR is then determined by finding the discount rate that sets the NPV to zero. This is often done iteratively using trial-and-error or through specialized software tools.

The IRR represents the rate of return or profitability of the project. It indicates the percentage rate at which the project's cash inflows grow over time, taking into account the time value of money. If the calculated IRR is higher than the company's required rate of return or cost of capital, the project is generally considered acceptable and financially viable. When comparing multiple investment opportunities, the project with the highest IRR is typically preferred since it implies a higher rate of return. However, it is important to consider other factors such as project size, risk, and the absolute value of cash flows alongside IRR.

Additionally, IRR may have limitations in certain situations, such as when cash flows change signs multiple times or when comparing projects with different cash flow patterns. One consideration with IRR is that it assumes that cash flows generated by the project will be reinvested at the same rate as the IRR itself. This assumption may not always be realistic, especially when the IRR is significantly higher than the cost of capital. While IRR is a valuable tool for evaluating investments, it should be used alongside other capital budgeting techniques such as NPV and complemented with qualitative analysis to make well-informed investment decisions.

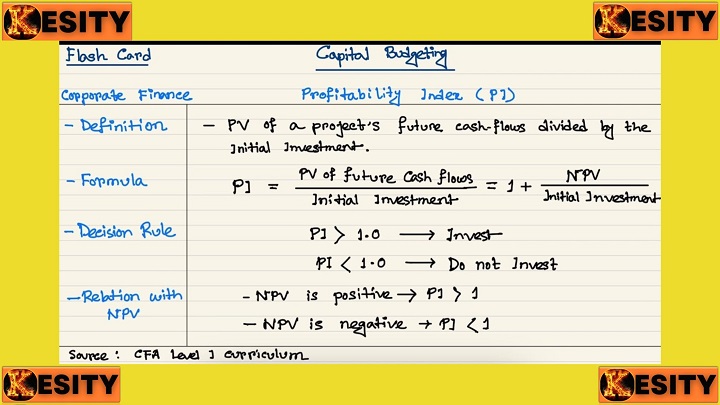

Profitability Index (PI)

The profitability index (PI), also known as the profit investment ratio (PIR) or the benefit-cost ratio (BCR), is a capital budgeting technique used to assess the profitability of an investment project. It measures the relationship between the present value of cash inflows and the present value of cash outflows associated with the project. To calculate the profitability index, the present value of expected cash inflows is divided by the present value of cash outflows. The present value of cash flows is determined by discounting future cash flows using an appropriate discount rate, typically the company's cost of capital.

A profitability index greater than 1 indicates that the present value of cash inflows exceeds the present value of cash outflows, resulting in a positive net present value (NPV). This suggests that the project is expected to generate more value than the initial investment and is considered financially viable. The higher the profitability index, the greater the expected profitability of the project.

The profitability index helps in comparing and ranking investment projects. When evaluating multiple projects, the one with the highest profitability index is generally preferred, as it represents the highest expected return relative to the initial investment. However, it is important to consider other factors such as project risks, strategic alignment, and funding availability alongside the profitability index. It's worth noting that the profitability index is particularly useful when there are capital rationing constraints, where the company has limited funds available for investment. In such cases, the profitability index helps in selecting projects that provide the most significant return on investment relative to the resources invested.  While the profitability index is a useful capital budgeting technique, it is important to interpret its results in conjunction with other financial metrics and qualitative factors to make informed investment decisions.

While the profitability index is a useful capital budgeting technique, it is important to interpret its results in conjunction with other financial metrics and qualitative factors to make informed investment decisions.

Discounted Payback Period

The discounted payback period is a capital budgeting technique that improves upon the traditional payback period by incorporating the time value of money. It calculates the time required to recover the initial investment based on the discounted cash flows rather than the undiscounted cash flows. To calculate the discounted payback period, the expected cash inflows are discounted to their present value using an appropriate discount rate, such as the company's cost of capital.

The cumulative discounted cash inflows are then tracked over time until they equal or exceed the initial investment. Unlike the simple payback period, which only considers the timing of cash flows without considering their present value, the discounted payback period accounts for the time value of money. By discounting the cash flows, it recognizes that a dollar received in the future is worth less than a dollar received today due to factors like inflation and the opportunity cost of capital. The discounted payback period provides a more comprehensive assessment of the time required to recover the initial investment because it considers the timing and discounted value of cash flows.

This technique helps address the limitations of the simple payback period, which does not account for the time value of money or consider cash flows beyond the payback period. It is important to note that the discounted payback period, like the simple one, does not capture the project's profitability beyond the payback period. Therefore, it should be used in conjunction with other capital budgeting techniques, such as net present value (NPV) or internal rate of return (IRR), to comprehensively assess an investment project. By incorporating the time value of money, the discounted payback period provides decision-makers with additional insights into the project's cash flow recovery timeline, helping them assess liquidity and risk associated with the investment.

Scenario Analysis

Scenario analysis is a valuable capital budgeting technique used to evaluate the potential impact of different scenarios on future cash flows. It involves creating and analyzing multiple scenarios based on varying assumptions about key variables that can affect the project's performance. The purpose of scenario analysis is to understand the range of possible outcomes and associated risks for a particular investment project. Decision-makers consider various factors such as sales growth, cost structure, market conditions, competition, regulatory changes, and technological advancements.

Different scenarios are constructed based on different combinations of these factors, representing various plausible future situations. The expected cash inflows and outflows are estimated for each scenario, considering the specific assumptions associated with that scenario. This allows decision-makers to assess the project's financial performance under different conditions. By evaluating the cash flows under multiple scenarios, decision-makers gain insights into the project's sensitivity to different factors and the potential risks involved. They can identify the best-case, worst-case, and most likely scenarios, helping them make more informed investment decisions.

Scenario analysis helps decision-makers understand the potential variability and uncertainties associated with the investment project. It allows them to assess the project's resilience to adverse conditions, identify potential risks and opportunities, and make contingency plans accordingly. While scenario analysis provides valuable insights, it is important to note that it relies on assumptions and forecasts that may not accurately predict the future. Therefore, scenario analysis should be used for risk assessment and decision-making, along with other capital budgeting techniques like NPV and IRR, and should be complemented with qualitative analysis and expert judgment. Overall, scenario analysis enables decision-makers to better understand the potential outcomes and associated risks of an investment project, facilitating more robust and informed decision-making.

Sensitivity Analysis

Sensitivity analysis is a vital tool in capital budgeting that allows decision-makers to understand the sensitivity of project outcomes to changes in key variables. It involves systematically varying one variable at a time while keeping all other factors constant to assess the impact on cash flows and the overall viability of the project. Sensitivity analysis aims to identify the variables that have the most significant influence on cash flow predictions and project outcomes. By examining the project's sensitivity to changes in these variables, decision-makers can gain insights into the project's robustness and potential risks. Here's an overview of the steps involved in conducting sensitivity analysis:

- Identify key variables: Start by identifying the key variables expected to substantially impact the project's cash flows. These variables can vary depending on the nature of the project but often include factors such as sales volume, pricing, costs, interest rates, inflation, and exchange rates.

By identifying the variables that have the greatest influence on cash flows, decision-makers can prioritize their attention and efforts to manage those risks effectively. It's important to note that sensitivity analysis has limitations. It assumes that the tested variables can be changed independently, which may not always be true in real-world scenarios. Additionally, sensitivity analysis does not account for potential interactions between variables, which can also affect project outcomes. Overall, sensitivity analysis is a valuable technique for understanding the impact of key variables on project viability. It provides decision-makers with insights into the potential risks and uncertainties associated with the project, enabling them to make more informed investment decisions and develop appropriate risk mitigation strategies.  These capital budgeting techniques assist in predicting future cash flows by considering factors such as the time value of money, risk, and various scenarios. It is important to note that these techniques have their limitations and should be used in conjunction with other qualitative and quantitative factors to make informed investment decisions.

These capital budgeting techniques assist in predicting future cash flows by considering factors such as the time value of money, risk, and various scenarios. It is important to note that these techniques have their limitations and should be used in conjunction with other qualitative and quantitative factors to make informed investment decisions.