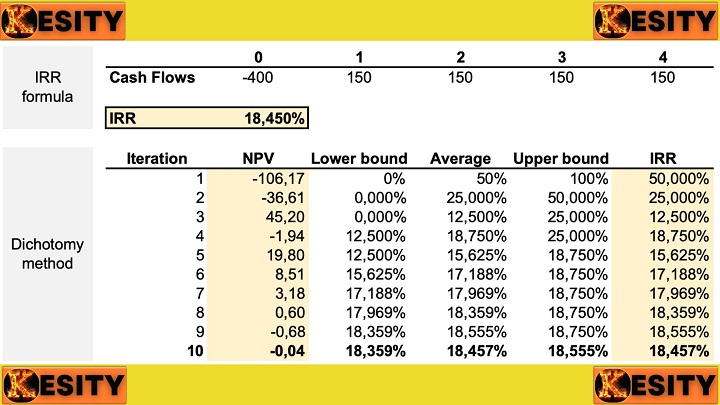

Capital budgeting is a crucial process that involves evaluating and selecting investment projects that provide the highest return to a company's shareholders. Several methods are available for capital budgeting, and one widely used technique is the Internal Rate of Return (IRR). The IRR offers several advantages as a method for capital budgeting, which we will explore in detail in this article. The IRR is a powerful tool that enables decision-makers to assess the profitability and feasibility of investment projects. Let's look into the advantages of IRR and understand why it is favored by financial experts. The IRR method offers simplicity and ease of understanding, making it accessible to both financial experts and non-experts. Unlike other complex methods like the net present value (NPV), which requires extensive calculations and discounted cash flow analysis, the IRR provides a single percentage figure that represents the rate of return on an investment. This straightforward interpretation of the IRR makes it easier for decision-makers to grasp the potential profitability of an investment project. One significant advantage of the IRR method is its ability to account for the time value of money. By discounting future cash flows to their present value, the IRR incorporates the concept that a dollar received in the future is worth less than a dollar received today. This consideration is essential in capital budgeting, as it enables decision-makers to compare the profitability of different projects accurately. The time value of money is a fundamental concept in finance that recognizes the notion that the value of money changes over time. A dollar received today is worth more than the same dollar received in the future due to its potential earning capacity and inflationary factors. The IRR method takes this principle into account, making it a valuable tool in capital budgeting. Here's an example to illustrate the advantage of considering the time value of money in IRR calculations: Suppose a company is considering two investment projects: Project A and Project B. Project A requires an initial investment of $100,000 and is expected to generate cash inflows of $30,000 per year for five years. Project B requires an initial investment of $150,000 and is expected to generate cash inflows of $40,000 per year for five years. To evaluate the profitability of these projects, the company calculates the IRR for each project. To calculate the IRR, the cash inflows from each project are discounted to their present value using an appropriate discount rate. Let's assume a discount rate of 10% for this example: Year 1: $30,000 / (1 + 0.10)^1 = $27,273 Year 2: $30,000 / (1 + 0.10)^2 = $24,794 Year 3: $30,000 / (1 + 0.10)^3 = $22,540 Year 4: $30,000 / (1 + 0.10)^4 = $20,491 Year 5: $30,000 / (1 + 0.10)^5 = $18,628 Year 1: $40,000 / (1 + 0.10)^1 = $36,364 Year 2: $40,000 / (1 + 0.10)^2 = $33,058 Year 3: $40,000 / (1 + 0.10)^3 = $30,051 Year 4: $40,000 / (1 + 0.10)^4 = $27,319 Year 5: $40,000 / (1 + 0.10)^5 = $24,841 Next, the present values of the cash inflows are summed up for each project: $27,273 + $24,794 + $22,540 + $20,491 + $18,628 = $113,726 Project B: $36,364 + $33,058 + $30,051 + $27,319 + $24,841 = $151,633 Using the IRR formula, the company can calculate the IRR for each project by finding the discount rate that equates the present value of cash inflows to the initial investment: $113,726 / $100,000 = 1.13726 or 13.73% IRR for Project B: $151,633 / $150,000 = 1.01089 or 1.09% Based on the IRR calculations, Project A has an IRR of 13.73%, while Project B has an IRR of 1.09%. Since the IRR of Project A is higher than the company's cost of capital, it indicates that Project A has a higher rate of return and is more financially attractive. By considering the time value of money, the IRR method allows decision-makers to compare projects on an equal footing, accounting for the impact of cash flows over time. This advantage ensures that investments with higher IRRs, which reflect higher rates of return, are prioritized, leading to more effective capital budgeting decisions. The IRR allows decision-makers to measure the profitability of an investment project. It calculates the discount rate at which the present value of cash inflows equals the initial investment cost. If the IRR is higher than the company's cost of capital or the desired rate of return, it signifies that the project is profitable and adds value to the organization. This advantage helps decision-makers prioritize investment opportunities and allocate resources efficiently. Measuring project profitability is a critical aspect of capital budgeting, and the IRR method excels in providing decision-makers with a clear indication of a project's financial viability. By calculating the IRR, decision-makers can assess whether an investment project generates returns that exceed the company's cost of capital or the desired rate of return. Let's explore this advantage in more detail with an example: A company is considering investing in a new manufacturing facility. The project requires an initial investment of $5 million and is expected to generate cash inflows of $1 million per year for five years. To evaluate the project's profitability, the company calculates the IRR. Using the IRR formula, the company determines the discount rate at which the present value of the cash inflows equals the initial investment: $1,000,000 / (1 + r)^1 Year 2: $1,000,000 / (1 + r)^2 Year 3: $1,000,000 / (1 + r)^3 Year 4: $1,000,000 / (1 + r)^4 Year 5: $1,000,000 / (1 + r)^5 The present values of the cash inflows are then summed up: PV = [$1,000,000 / (1 + r)^1] + [$1,000,000 / (1 + r)^2] + [$1,000,000 / (1 + r)^3] + [$1,000,000 / (1 + r)^4] + [$1,000,000 / (1 + r)^5] The IRR is determined by finding the discount rate that makes the present value of the cash inflows equal to the initial investment: IRR: PV = $5,000,000 Based on the calculations, let's assume the IRR is determined to be 10%. If the company's cost of capital is 8%, the IRR of 10% indicates that the project generates a higher rate of return than the company's cost of capital. This signifies that the project is profitable and adds value to the organization. By measuring project profitability, the IRR method allows decision-makers to prioritize investment opportunities effectively. Projects with higher IRRs are considered more financially attractive and are given preference over projects with lower IRRs. This advantage aids decision-makers in allocating resources efficiently and focusing on investments that have the potential to generate substantial returns. It is important to note that while the IRR measures project profitability, it does not provide information about the absolute value of the returns or the project's size. Therefore, it is crucial for decision-makers to consider other financial metrics, such as the net present value (NPV), in conjunction with the IRR to obtain a more comprehensive understanding of the investment's financial implications. In conclusion, the IRR method serves as a valuable tool for measuring project profitability in capital budgeting. By comparing the IRR to the company's cost of capital or desired rate of return, decision-makers can assess whether an investment project is financially viable and aligns with the organization's goals. This advantage enables decision-makers to make informed investment decisions, allocate resources effectively, and enhance the overall financial performance of the company. Another advantage of the IRR method is that it encourages sensitivity analysis. Sensitivity analysis involves examining how changes in key variables impact the project's financial viability. By manipulating the cash flow assumptions or adjusting the discount rate, decision-makers can assess the project's sensitivity to different scenarios. This analysis helps identify the critical factors that influence the project's profitability and aids in mitigating potential risks. The IRR method enables decision-makers to compare multiple investment projects efficiently. By calculating the IRR for each project, decision-makers can rank and prioritize projects based on their relative profitability. This advantage is particularly valuable when companies have limited resources and need to make strategic investment decisions. By comparing the IRRs of different projects, decision-makers can identify the most attractive investment opportunities and allocate resources accordingly. Capital rationing refers to the situation where a company has limited funds and needs to select the most promising investment projects. The IRR method is advantageous in capital rationing decisions as it helps identify projects that provide the highest returns per unit of investment. By selecting projects with higher IRRs, companies can optimize their resource allocation and maximize shareholder wealth. In situations of capital rationing, where a company has limited funds available for investment, the IRR method plays a vital role in supporting decision-making. By considering the advantage of the IRR method, companies can effectively allocate their limited capital to projects that offer the highest returns per unit of investment. When facing capital rationing, decision-makers need to carefully evaluate and prioritize investment projects to make the most efficient use of available resources. The IRR method becomes a valuable tool in this process. By calculating the IRR for each potential investment project, decision-makers can identify projects with higher rates of return relative to their investment requirements. Suppose a company has a capital budget of $10 million and is considering several investment projects. The IRR method can help in selecting the most promising projects based on their returns per unit of investment. Let's consider the following two investment options: Requires an investment of $4 million and has an IRR of 15%. Project B: Requires an investment of $8 million and has an IRR of 12%. To determine which project to pursue under capital rationing, decision-makers would assess the profitability of each project relative to the required investment. In this case, Project A offers a higher rate of return per unit of investment compared to Project B. Allocating $4 million to Project A and excluding Project B would result in a more efficient utilization of available capital. By prioritizing projects with higher IRRs, decision-makers ensure that limited funds are allocated to projects with the greatest potential for generating returns. This approach maximizes shareholder wealth by focusing on investments that deliver the most significant value for each dollar invested. It's important to note that capital rationing decisions should not solely rely on the IRR method. Other factors, such as the strategic fit, risk assessment, and the company's long-term objectives, should also be taken into consideration. However, the IRR method acts as a valuable tool for identifying projects that offer the most attractive returns in a capital-constrained environment. In summary, the IRR method supports capital rationing decisions by enabling decision-makers to identify investment projects that provide higher returns per unit of investment. By allocating limited funds to projects with higher IRRs, companies can optimize their resource allocation and maximize shareholder wealth. However, it is crucial to consider other factors alongside the IRR, such as strategic alignment and risk assessment, to make well-informed capital rationing decisions. Unlike some other capital budgeting methods that focus solely on the initial investment and payback period, the IRR method considers the entire cash flow timeline of a project. It accounts for all cash inflows and outflows over the project's lifespan, providing decision-makers with a comprehensive view of the project's profitability and financial impact. This advantage allows decision-makers to assess the long-term sustainability and viability of an investment project. Considering the entire cash flow timeline is a significant advantage of the IRR method in capital budgeting. While other methods may only focus on the initial investment and the payback period, the IRR method takes into account all cash inflows and outflows throughout the project's lifespan. This comprehensive assessment provides decision-makers with a holistic view of the project's profitability and financial impact. Let's explore this advantage further with an example: A company is considering investing in a renewable energy project that involves building a solar power plant. The project has an expected lifespan of 20 years and requires an initial investment of $10 million. Over the 20-year period, the project is expected to generate annual cash inflows of $2 million. Using the IRR method, decision-makers would analyze the entire cash flow timeline to determine the project's financial viability. The calculation involves discounting the cash inflows and outflows to their present values and finding the discount rate that makes the net present value (NPV) of the project equal to zero. Considering the cash inflows of $2 million per year for 20 years, the present values of these cash flows are calculated using the appropriate discount rate: $2,000,000 / (1 + r)^1 Year 2: $2,000,000 / (1 + r)^2 ... Year 20: $2,000,000 / (1 + r)^20 The present values of the cash inflows are then summed up: PV = [$2,000,000 / (1 + r)^1] + [$2,000,000 / (1 + r)^2] + ... + [$2,000,000 / (1 + r)^20] The IRR is determined by finding the discount rate that makes the NPV of the project equal to zero: NPV = PV - Initial Investment = 0 By considering the entire cash flow timeline, the IRR method provides decision-makers with a comprehensive evaluation of the project's financial viability. If the calculated IRR is higher than the required rate of return or the company's cost of capital, it indicates that the project generates positive returns and is financially attractive over its lifespan. This advantage of the IRR method allows decision-makers to assess the long-term sustainability and viability of an investment project. By considering all cash inflows and outflows, decision-makers can evaluate the project's profitability over time, identify potential risks or challenges, and make informed investment decisions. However, it is important to note that the IRR method assumes that cash flows generated by the project are reinvested at the IRR itself, which may not always be realistic. Therefore, it is recommended to use the IRR method in conjunction with other financial metrics, such as the net present value (NPV), to obtain a more comprehensive understanding of the project's financial implications. Therefore, the IRR method's consideration of the entire cash flow timeline in capital budgeting provides decision-makers with a comprehensive view of a project's profitability and financial impact. By assessing all cash inflows and outflows over the project's lifespan, decision-makers can evaluate the project's long-term sustainability, identify potential risks, and make well-informed investment decisions. In conclusion, the Internal Rate of Return (IRR) offers several advantages as a method for capital budgeting. Its simplicity, consideration of the time value of money, ability to measure project profitability, encouragement of sensitivity analysis, facilitation of project comparison, support for capital rationing decisions, and consideration of the entire cash flow timeline make it a valuable tool for decision-makers. By leveraging the advantages of IRR, companies can make informed investment decisions, maximize profitability, and create value for their stakeholders.Simplicity and Ease of Understanding

Considers the Time Value of Money

Example

For Project A

For Project B

Project A

IRR for Project A

Measures Project Profitability

Example

Year 1

Encourages Sensitivity Analysis

Facilitates Comparison of Projects

Supports Capital Rationing Decisions

Example

Project A

Read Also: Non-Financial Factors in NPV Calculations

Considers the Entire Cash Flow Timeline

Example

Year 1

Read Also: Role of Profitability Index in Capital Budgeting