Introduction

In the world of finance and investment, capital budgeting is a crucial process that helps businesses make informed decisions regarding their long-term investments. One of the key metrics used in this process is the Profitability Index (PI). The role of the Profitability Index in capital budgeting cannot be overstated, as it serves as a powerful tool for evaluating the potential profitability of investment projects. This essay will explore the various aspects of the Profitability Index and its significance in the capital budgeting process.

Understanding Capital Budgeting

- Capital budgeting is the process of evaluating potential investments and projects for long-term benefits and growth.

- The objective of capital budgeting is to choose projects that align with the company's strategic goals and offer positive future cash flows and attractive returns on investment.

- The evaluation process involves projecting future cash inflows and outflows and discounting them to their present value to account for the time value of money.

- Return on Investment (ROI) is a crucial factor in capital budgeting, as businesses seek projects with favorable returns that exceed the cost of capital.

- Non-financial factors, such as market conditions, technology advancements, regulatory changes, and environmental impact, are also considered in the decision-making process.

- Efficient allocation of resources is essential to maximize wealth and create value for stakeholders.

- Continuous monitoring and evaluation of implemented projects are necessary to ensure they remain aligned with strategic objectives and deliver expected benefits.

What is the Profitability Index?

The Profitability Index, also known as the

Profit Investment Ratio (PIR) or Benefit-Cost Ratio (BCR), is a financial metric used to assess the feasibility and profitability of investment projects. It is calculated by dividing the present value of cash inflows from a project by the present value of cash outflows. The result is a ratio that helps decision-makers determine the project's profitability in relation to the initial investment.

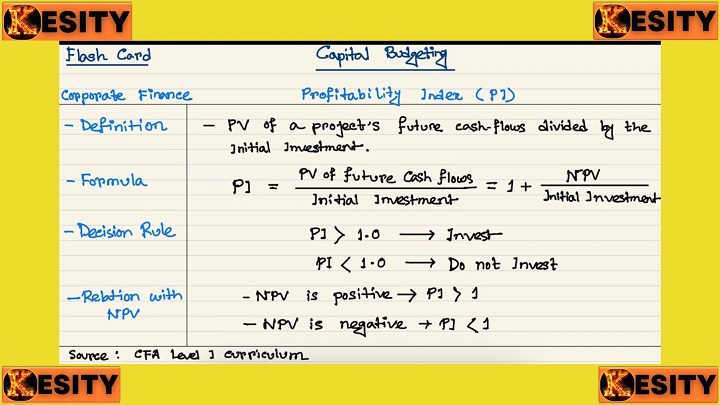

- The Profitability Index (PI) is a financial metric used to evaluate the profitability and feasibility of investment projects.

- Also known as the Profit Investment Ratio (PIR) or Benefit-Cost Ratio (BCR), it aids decision-makers in making informed choices about potential investments.

- The PI is calculated by dividing the present value of expected cash inflows from a project by the present value of cash outflows associated with the investment.

- A PI greater than 1 indicates that the project's present value of cash inflows exceeds the present value of cash outflows, suggesting a profitable investment.

- A PI equal to 1 means that the present value of cash inflows is equal to the present value of cash outflows, indicating a break-even point.

- A PI less than 1 implies that the present value of cash inflows is lower than the present value of cash outflows, signaling a potential loss or unprofitable investment.

- The Profitability Index complements other capital budgeting metrics like Net Present Value (NPV) and Internal Rate of Return (IRR) in evaluating investment opportunities.

- It provides decision-makers with a relative measure of profitability, enabling them to compare and prioritize different projects based on their potential returns.

- The PI is particularly useful when companies face capital constraints and need to rank projects to allocate resources optimally.

- A higher PI suggests a more favorable investment opportunity, as it indicates a higher potential return relative to the initial investment.

The Role of Profitability Index in Capital Budgeting

-

Project Selection Criteria:

-

- The Profitability Index is a pivotal criterion for project selection in capital budgeting, aiming to maximize wealth and create value for shareholders.

- It complements NPV analysis by evaluating the ratio of present value of cash inflows to the present value of cash outflows.

- Decision-makers use the Profitability Index to rank and prioritize projects based on their relative profitability.

- Projects with a higher PI are preferred, as they offer better returns and contribute more significantly to the company's overall financial well-being.

- The Profitability Index aids businesses in making informed investment decisions that align with their strategic goals and objectives.

- By considering the relative profitability of investment projects, the PI helps optimize resource allocation and capital utilization.

- It provides a quantitative measure of each project's potential to generate positive cash flows and contribute to long-term financial growth.

- The Profitability Index enables businesses to identify and select projects that are most likely to yield positive returns on investment.

- It serves as a valuable tool for decision-makers to assess the financial viability and profitability of various investment opportunities.

- Overall, the Profitability Index enhances the capital budgeting process, ensuring that businesses make prudent and profitable investment choices.

-

- Comparative Analysis: The Profitability Index facilitates comparative analysis between multiple investment opportunities in the context of capital budgeting.

- Limited Resources: Businesses often face capital constraints and must choose between various investment projects with limited resources.

- Informed Choices: The Profitability Index allows decision-makers to make well-informed choices by evaluating the PI of each project.

- Most Attractive Opportunities: Management can determine the most attractive investment opportunities based on their respective PI values.

- Optimal Resource Allocation: The PI assists in optimal resource allocation, directing capital towards projects with the highest potential for profitability.

- Maximizing Returns: By selecting projects with higher PI values, businesses can aim to maximize returns and achieve better financial outcomes.

- Strategic Decision-Making: The comparative analysis facilitated by the PI contributes to strategic decision-making in capital budgeting.

- Aligning with Goals: Companies can align investment decisions with their strategic goals and objectives through PI evaluation.

- Mitigating Risks: The PI aids in mitigating risks associated with investment choices, ensuring better allocation of resources.

- Improving Efficiency: The Profitability Index enhances efficiency in the capital budgeting process by streamlining investment evaluations.

-

Time Value of Money Consideration

-

- Time Value of Money Consideration: The Profitability Index considers the Time Value of Money (TVM) in evaluating investment decisions.

- Discounting Future Cash Flows: The PI discounts future cash flows to their present value, adjusting for the impact of inflation and interest rates.

- Consistent Evaluation: By discounting cash flows, the PI ensures a consistent evaluation of all inflows and outflows over the project's lifespan.

- Comparing Projects: Considering TVM enables easy comparison of different projects with varying cash flow timings.

- Changing Value of Money: TVM acknowledges the changing value of money over time, reflecting its decreasing purchasing power.

- More Accurate Assessment: Accounting for TVM enhances the accuracy of the project's profitability assessment.

- Long-Term Perspective: The PI's TVM consideration provides a long-term perspective on investment returns.

- Informed Decision-Making: Factoring in TVM helps decision-makers make informed choices about project feasibility and viability.

- Investment Risk: TVM consideration aids in understanding and mitigating investment risk associated with cash flows in the future.

- Sensitivity Analysis: Sensitivity analysis of cash flows under TVM provides insights into project resilience to market fluctuations.

-

- Efficiency Indicator: The Profitability Index serves as an efficiency metric, measuring returns per unit of investment.

- Positive Returns: A PI greater than 1 indicates positive returns, signaling a potentially lucrative opportunity.

- Financial Viability: A PI less than 1 implies a negative return, suggesting the investment may not be financially viable.

- Optimal Resource Allocation: The PI helps in optimal resource allocation by prioritizing projects with higher efficiency.

- Growth and Prosperity: Focusing on high PI projects contributes to the company's growth and prosperity.

- Profit Maximization: Businesses aim to maximize profits, and the PI aids in identifying projects that align with this objective.

- Comparing Profitability: The PI allows easy comparison of projects' profitability and efficiency.

- Ranking Projects: Decision-makers can rank projects based on their efficiency, making informed investment choices.

- ROI Evaluation: The PI provides insights into the return on investment for different projects.

- Risk-Adjusted Efficiency: Combining PI with risk assessment enables evaluating efficiency while considering project risks.

-

- Risk Assessment: The Profitability Index aids in risk assessment during Capital Budgeting.

- Uncertainty and Variability: PI considers the uncertainty and variability of cash flows in projects.

- Predictable Cash Flows: Projects with higher PI often have more predictable cash flows.

- Risk-Averse Situations: Predictable cash flows are preferred in risk-averse situations.

- Prudent Decision-Making: Understanding project risks helps in making prudent investment decisions.

- Alignment with Risk Tolerance: Management aligns investments with the company's risk tolerance.

- Financial Objectives: Assessing risk ensures projects align with financial objectives.

- Mitigating Potential Losses: Lower-risk projects may be favored to mitigate potential losses.

- Diversification: Evaluating risk aids in diversifying investment portfolios.

- Comprehensive Decision-Making: Combining risk assessment with other metrics leads to comprehensive decision-making.

-

Complementing Other Metrics

-

- Complementing Other Metrics: PI works best when combined with other capital budgeting metrics.

- Comprehensive View: Relying solely on PI may not provide a comprehensive assessment of projects.

- Holistic Evaluation: Combining PI with NPV, IRR, and Payback Period gives a holistic evaluation.

- Financial Feasibility: The metrics together assess the financial feasibility of projects.

- Informed Decision-Making: Using multiple metrics leads to well-informed investment decisions.

- Aligning with Objectives: Evaluating projects from different angles aligns with strategic objectives.

- Identifying Consistency: Consistency among metrics reinforces project viability.

- Identifying Divergence: Divergent results among metrics may signal potential risks or benefits.

- Strategic Resource Allocation: Comprehensive evaluation aids in optimal resource allocation.

- Minimizing Biases: Relying on multiple metrics reduces potential biases in decision-making.

Conclusion

- The Profitability Index is crucial in guiding businesses towards profitable investment decisions in capital budgeting.

- It aids in project selection by providing a relative measure of profitability, allowing decision-makers to rank and prioritize investment opportunities.

- The Profitability Index facilitates comparative analysis, enabling businesses to assess and compare multiple investment projects.

- It considers the time value of money by discounting future cash flows, ensuring a consistent evaluation of project profitability over time.

- The Profitability Index serves as an efficiency indicator, revealing the returns generated per unit of investment.

- It aids in risk assessment by considering the uncertainty and variability of cash flows, helping decision-makers make informed choices in risk-averse situations.

- The Profitability Index complements other capital budgeting metrics such as Net Present Value (NPV) and Internal Rate of Return (IRR), providing a comprehensive view of project viability.

- By incorporating the Profitability Index into decision-making processes, businesses can optimize their capital allocation and enhance financial performance.

- Utilizing the Profitability Index helps companies align investments with strategic goals, driving long-term profitability and growth prospects.

- Overall, the Profitability Index is an indispensable tool for effective capital budgeting, empowering businesses to make informed and successful investment decisions.

Comments are closed!